Calculate R&D tax credits with Gusto

This article is for admins who want Gusto to calculate and apply their federal R&D tax credit.

The Federal Research and Development (R&D) Tax Credit rewards US companies that invest in technological innovation. You can claim this federal tax credit for qualified research and development (R&D) costs.

A Qualified Small Business (QSB) can use up to $500,000 in R&D tax credits each year to pay the company portion of payroll taxes (Social Security and Medicare). Your business qualifies as a QSB if it has generated revenue for less than five years and earned less than $5,000,000 in gross revenue in the tax year. Gross revenue includes sales, interest, rents, royalties, dividends, and other forms of income.

Read the FAQs to learn more about identifying and claiming R&D tax credits with Gusto, or book a call with us here.

Complete the qualification survey to find out if you're eligible for Gusto R&D tax credits.

To apply for Gusto R&D tax credits:

Go to Taxes & Compliance.

Click Tax incentives.

Under Available credits, in the Research & development tax credit tile, click See if I qualify.

Fill out the survey.

Click Save and continue.

If you qualify for R&D tax credits, click Continue to Gusto R&D.

Our team will review your eligibility, examine your payroll data, calculate your credit, and provide an estimated credit for your review and approval.

You can increase your credit by uploading more expenses, like contractor costs and supplies. Our Gusto R&D Credit Specialists are available by email or Zoom to answer your questions.

Application timeline for the R&D tax credit

You can expect to spend about two hours completing your R&D tax credit application.

You'll use Gusto's online platform to get prequalified. Share details about your product, technical challenges, and the testing process. Then connect or upload your expenses and a few prior tax returns. We calculate your credit, prepare documentation, and help you file Form 6765 with your annual tax return.

To qualify for the R&D tax credit, companies must meet all four requirements in the Internal Revenue Service (IRS) four-part test.

The four requirements are:

Permitted purpose: You develop a new or improved business component (product, process, software, formula, technique, or invention) for sale, license, or lease.

Technological in nature: Your work relies on hard science, like engineering, physical sciences, or computer science.

Eliminate uncertainty: Your work eliminates uncertainty about how to develop or improve a product or process.

Process of experimentation: You test multiple methods to achieve a result.

Make sure you document your research activities in case your company needs to defend your credits.

Before you start your application, gather your company details, wage information, expenses, and tax forms.

Our team will use this information to review your eligibility, examine your payroll data, calculate your credit, and share an estimated credit for your approval. Providing tax returns and reconciling expenses may increase your credit.

Our Gusto R&D Credit Specialists are available to answer your questions throughout the process.

Share your first year of R&D activities, first year of revenue, and tax year-end date. You also need:

Company type for LLC: Your Limited Liability Company (LLC) type depends on how the IRS taxes your business. Choose the option that matches your tax filing:

Single-member LLCs are taxed as sole proprietorships and file Form 1040 with Schedule C for federal tax filing.

Enter "Sole Proprietorship" when onboarding.

Multi-member LLCs are taxed as partnerships.

Enter S-Corp if your business files Form 1120-S.

Enter "General Partnerships" if your business files Form 1065.

LLCs can be taxed as C Corporations.

Enter "C-Corp" if your business files Form 1120.

Your company's FEIN: Find your Federal Employer Identification Number (FEIN) in the top-right corner of your Corporate Federal Tax Return form.

If your business has had multiple EINs, tell the team so we can calculate your credit accurately. Include any FEIN changes in the Onboarding Notes section before you submit.

Parent company and subsidiary: A parent company controls or owns at least 51% of another company (the subsidiary). The IRS calls this corporate structure a control group.

Accounting basis: This refers to how you maintain your books or general ledgers. Your tax return also lists this information.

Important: Close and reconcile your accounting books and ledgers before we include these expenses in your calculation so you get a complete and accurate tax credit.

State of business: Enter the state where your business is physically located.

Impact of revenue and profitability: Your revenue and profitability status determine how you can use your R&D credits.

Example: Startups with annual gross receipts of less than $5 million and less than five years with gross receipts may have different options for credit use.

Pro Tip: When we ask "Was your company profitable in 2025?", we want to know if your business expects to pay the IRS a tax liability when filing. This impacts how you use your R&D tax credits. If you're unsure if you'll owe a tax liability when filing, ask your tax preparer.

For Gusto customers, wages and contractor payments made through Gusto automatically import through the Gusto Application Programming Interface (API). Our software recommends percentages based on similar companies to yours in employee size and industry. During onboarding, you can review and adjust the software's suggested percentages for more accuracy.

If you have W-2s for part of the year under review, email [email protected] for a secure link to provide that information.

Important: For R&D wages and expenses to qualify for this credit, you must conduct all related R&D activity on US soil. This includes US territories like Puerto Rico and Guam. The IRS calculates all contractor expenses using 65% of the total qualified research expenses. This is compliant with IRS regulations outlined in Internal Revenue Code (IRC) Section 41(b)(3)(A). This does not apply to supply or hosting expenses.

We use expenses like contractor fees, hosting costs, patent-related legal fees, and supplies related to R&D to calculate your R&D tax credit. Providing expense data helps increase your total R&D tax credit by capturing additional qualifying spend, including contractors, software/hosting, and supplies.

You have two ways to provide your expenses

Option 1: Enter expenses directly (recommended)

Directly input your qualifying expenses by category — no accounting integration required. As you enter amounts, your credit estimate updates in real time so you can immediately see the impact.

Option 2: Import your general ledger

Import expenses through our Codat integration. We support direct connections with QuickBooks Online, QuickBooks Desktop, Xero, and FreshBooks. Our team will review your ledger to identify qualifying expenses.

Important: For R&D wages and expenses to qualify for this credit, you must conduct all related R&D activity on US soil. This includes US territories such as Puerto Rico and Guam. If your contractors meet this criteria, but are not qualified, email [email protected] to provide more information regarding their scope of work and time spent on R&D.

Submit four years of prior federal tax returns (complete filed copies). This helps determine your average annual gross receipts, which is crucial for accurate R&D credit calculations.

If you're using Gusto for the first time to claim R&D tax credits but have claimed them in prior years, our team needs these prior filings when calculating your credits for the current tax year.

We aim to simplify the R&D tax credit application process, but complexities like entity conversions, Fiscal Year Ends, and control groups may impact an accurate calculation. When submitting your application, provide accurate details about these complexities.

Entity conversions

An entity conversion changes your business's legal structure or type. This may include updates to the incorporation date, business name, or FEIN. When claiming R&D tax credits, provide the initial incorporation date and note any changes. These changes can affect credit calculations.

Example: If an S-Corp incorporated on January 1, 2024, and converted to a C-Corp on October 1, 2025, tax filings would reflect three periods:

January 1, 2024–December 31, 2024 (Filed on Form 1120-S)

January 1, 2025–September 30, 2025 (Filed on Form 1120-S)

October 1, 2025–December 31, 2025 (Filed on Form 1120)

In this case, use the initial incorporation date (January 1, 2024) during the onboarding process. Document any changes, including dates before and after the conversion, in the Onboarding Notes section.

For instance, you might note:

"My business changed from an S-Corp to a C-Corp in 2025. The original incorporation date was January 1, 2024, and the final Form 1120-S was filed for the period ending September 30, 2025. The C-Corp conversion began on October 1, 2025, with a year-end of December 31, 2025."

Fiscal Year Ends

A Fiscal Year End (FYE) is the final day of a company's 12-month accounting period used for financial reporting and tax purposes. This is when the company closes its books, prepares financial statements, and assesses its annual performance. If a company's Fiscal Year End aligns with the calendar year-end, it falls on December 31.

If the company has had more than one FYE in the life of the business, our team needs to know any prior year-end dates that were previously applicable. We recommend notifying our team in the Onboarding Notes section before you submit your application.

For instance, you might note:

"My business changed from a calendar year ending December 31 to a Fiscal Year End of September 30 in 2025."

Control groups

A control group, in the context of the R&D tax credit, refers to a collection of related businesses that the IRS treats as a single entity for tax purposes due to shared ownership or control. This affects how we calculate and apply the R&D tax credit, as we need to consider activities and expenses across all businesses in the control group. Control groups can be structured in a Parent/Child format or a Brother/Sister grouping. Be prepared to provide information about the other businesses, like tax returns, wages, and expenses (should the IRS require a separate study).

If you believe your business may be part of a controlled group, answer "Yes" during onboarding when we ask if your business has a "Parent or Subsidiary."

Example 1: "A holding company owns my business. The holding company is US-based, does not perform any R&D activity, and does not incur additional expenses."

Example 2: "Another entity (Parent company) owns my business. The Parent company also owns other entities, but none of them/some of them perform R&D activity."

Qualified expenses are costs directly related to your research and development activities. These expenses help increase your total R&D tax credit.

We calculate qualified wages based on your employee's contribution to R&D efforts. The time each employee spends on R&D activities determines what percentage of their salary qualifies for the R&D tax credit.

We use other qualified expenses to help increase your total R&D tax credit. These expenses provide insight into the contractors and supplies that qualify for R&D credit.

R&D tax credit calculation methods

There are a few methods of calculating the credit:

Regular method

We calculate the base amount by averaging annual gross receipts over the four years before the calculation year and multiplying it by a fixed base percentage. We then calculate the credit by subtracting the base amount from your total qualified research expenses (QRE), using the lower of the two figures, and multiplying by 20%.

You need the last four years of filed tax returns (or gross receipt numbers) and current-year QREs (wages and expenses).

Example: If the current calendar year is 2025, we need tax returns from 2020-2023 and wages and expenses from 2024 to calculate your credit.

Alternative Simplified Credit (ASC) method

This method uses QRE from the past three years to establish the base. We calculate the credit by halving the average QRE from the three prior years, subtracting it from the current year's QRE, and multiplying the result by 14%. If you have less than three years of QRE, the credit is 6% of the current year's qualified research expenditures.

You need three years of prior wages and expenses, and the current year's wages and expenses.

Example: If the current calendar year is 2025, we need wages and expenses from 2021-2024 to calculate your credit using the ASC method.

280C Election

Companies must reduce their capital account by the amount their R&D tax credits exceed their allowable R&D expense deduction. This prevents "double dipping," where you both credit and deduct R&D expenses. To avoid this reduction, make a 280C Election on a timely filed tax return. This reduces the R&D tax credit by the corporate tax rate and avoids the capital account adjustment.

Our Gusto R&D Credit Specialists can help determine which calculation method is right for your business.

How we calculate your R&D tax credit

To calculate your R&D tax credit:

We determine the calculation method based on factors like qualified research expenses, gross receipts, and the duration of your company's qualified R&D activities.

If you provide tax returns, we use the regular method. If not, we use the Alternative Simplified Credit method.

If you provide enough data for both methods, our team determines which one gives you a higher credit.

Our software reviews job titles and suggests percentages based on similar companies in your employee size and industry.

These are initial estimates that might need adjustments.

You review the estimated percentages and adjust them as needed.

If you're unable to make adjustments, click Book a Call in your R&D dashboard to speak with a member of our team.

The expense categories below qualify for the R&D tax credit. Understanding which expenses qualify helps you maximize your credit.

Wages: Salaries, wages, bonuses, and other pay for employees directly involved in conducting, supervising, or supporting qualified R&D activities. All qualified research activity must relate to developing the product or service you provide. Admin-related work does not qualify.

Substantially All Rule: This applies when we assign an 80% qualification to an employee's wages. The IRS allows the remaining 20% to qualify the employee at 100%. This typically applies to high-level technical roles, like engineers or scientists.

There are three categories of wage activities:

Direct Conduct/Research: Technical personnel (engineers, software developers, scientists, chemists) deeply involved in the development effort

Direct Supervision: First-line supervisors or managers directing or supervising the Direct Conduct development effort. This also includes executive personnel activities in directing the research.

Direct Support: Administrative assistants typing lab reports, clerks who clean lab equipment, or any employee who assists first-line technical personnel in conducting direct research activities. General admin, human resources, or finance do not qualify as Direct Support.

Examples of Qualified Direct Support:

Gathering technical information from customers and sharing this with the design team to help with development

Maintaining or cleaning the area where research happens, like cleaning lab equipment used in the research process, or IT activities to maintain a computer network that software engineers use to create code. Everyday janitorial tasks or IT troubleshooting do not qualify as direct support.

Gathering, categorizing, or recording test results from any test used in qualified research

Building any physical model used in qualified research

Supplies: Costs for purchasing materials, supplies, and equipment used and consumed (no longer viable after use) in R&D development and experiments. This includes raw materials, laboratory supplies (like beakers and test tubes), and testing materials.

Contract Research: Payments to third-party contractors or research organizations for conducting qualified research (universities, consulting services, research studies, prototype development, and independent contractors)

The research performed must meet these IRS criteria for qualified research:

Contractors must perform qualified research activities within US territories.

R&D tax credit rules require a 35% reduction ("haircut") on contract research costs to accommodate overhead expenses.

Unlike wages, the "Substantially All" rule does not apply to contract research. Contractors are typically more involved in the research process. For instance, if an employee (like a software developer) is typically qualified at 80%, when a contractor fills the same role, they should be considered 100% involved in the research process.

Leasing of Computers: Payments to an outside company that leases computers for use in qualified research. These payments must meet three requirements to be eligible for the R&D tax credit:

The computers are not located on your site.

Someone besides you owns the computers.

You are not the computer's primary user.

Hosting expenses may also qualify as the leasing of computers. Qualified hosting expenses can include services like Amazon Web Services, GitHub, and Atlassian. However, cloud-based email, marketing, and communication platforms do not qualify.

Section 174 of the Internal Revenue Code (IRC) explains how businesses should deduct their Research and Experimental (R&E) expenditures. R&E expenditures are R&D costs for activities that eliminate uncertainty about developing or improving a product.

Cost eligibility depends on the nature of the activity, not the product you develop or the level of technological advance.

The Tax Cuts and Jobs Act of 2017 (TCJA) amended Section 174. The amendment took effect with the 2022 tax year. This change caused confusion among many businesses about how it affected the Section 41 R&D credit and their tax bills.

For more details on Section 174 and updates, visit our blog article.

After we calculate your credits, you'll get an email asking you to review and approve your credits and payment. Log in to your R&D dashboard to review the calculated credits.

Before you approve, review the employee percentages of time spent on R&D activities and the qualified expenses our software has identified. If you need to make adjustments or have questions, connect with your Credit Specialist by clicking Book a Call or Send an Email in your R&D dashboard.

After you make adjustments (or if no adjustments are needed), approve your credits and payment options.

File your R&D tax credit with your federal income tax return. How you use your credit depends on whether you're a QSB, whether your company is profitable, and when you file.

The table shows what forms you need based on your business type.

C-Corp

S-Corp

Partnership

Sole Proprietor

Tax form

Form 1120

Form 1120-S

Form 1065

Form 1040, 1040-SR, Schedule C

Form 6765 (R&D form)

Yes

Yes

Yes

Yes

*Form 3800 (general business credit)

Yes, filed with Form 1120

Yes, filed with shareholder's Form 1040

Yes, filed with partner's Form 1040

Yes, filed with Sole Prop's Form 1040

*Schedule K-1

No

Yes (Schedule K-1, Form 1120-S)

Yes (Schedule K-1, Form 1065)

No

You use Form 6765 to claim R&D tax credits. File it with your federal income tax return. Gusto R&D Tax Credit Services calculates and prepares this form for you.

Companies claiming payroll offset

You can only claim a payroll tax offset on a timely filed return, including an extension. You cannot claim it on an amended return.

For a QSB, claim the payroll tax credit on your business tax return. You can start using these credits to offset employer-paid payroll taxes in the first quarter after you file your income tax return with Form 6765. Make sure the payroll tax election section is completed.

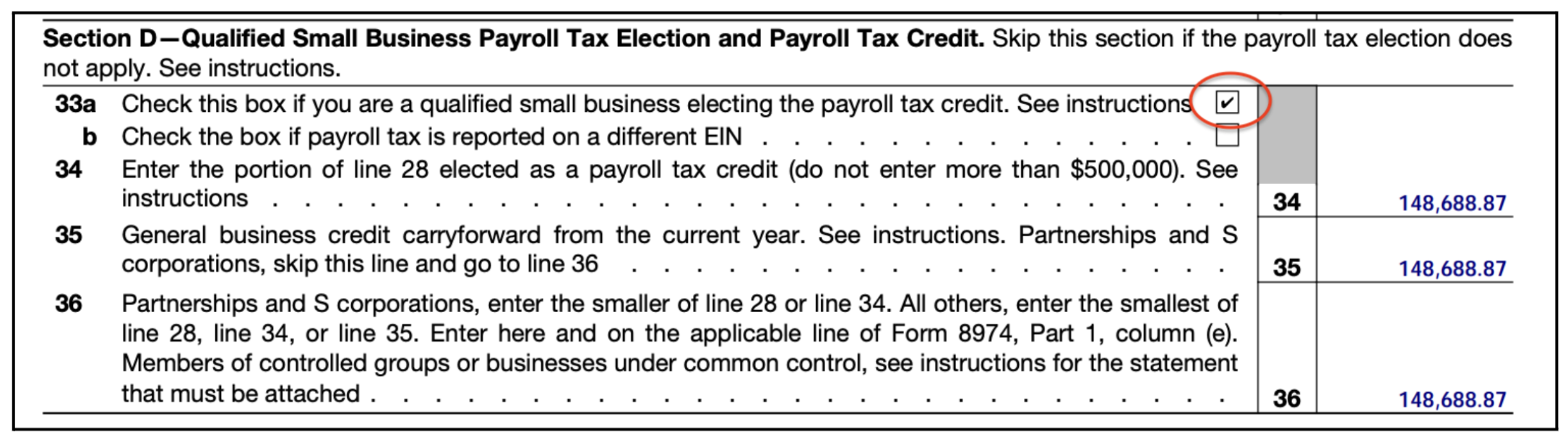

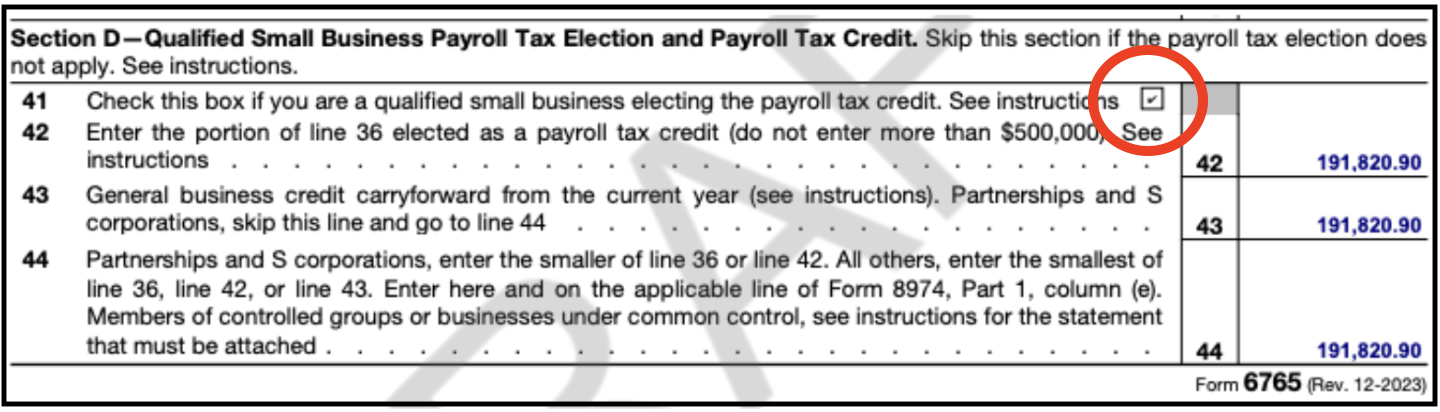

Form 6765 has a section at the bottom that allows a QSB to elect to apply some or all of the credit toward offsetting payroll taxes.

Important: If using the credit toward payroll tax, make sure Section D "Qualified Small Business Payroll Tax Election and Payroll Tax Credit" is filled out, including the box for payroll election:

For tax years 2023 and prior: Check Box 41.

For tax years 2024 and beyond: Check Box 33a.

If you do not check the box, the credit will be used toward income tax or carried forward toward future tax liabilities, depending on your company's profitability.

Profitable companies

If a profitable company files an on-time tax return without marking the payroll election section, the R&D credits are used as a liability tax offset at the time of filing. You can carry forward any unused credits to offset future income tax liability.

If you file the tax return on time without Form 6765, you must amend the return to include Form 6765 and claim the credits. As of January 10, 2022, the IRS requires a Declaration Statement for any refund claims. Gusto's R&D Tax Credit Team can help with this statement. If you want to amend a prior year's tax return to claim the R&D tax credit, email [email protected].

Non-profitable companies

If you were not profitable and filed an on-time tax return without the payroll election section, you can carry forward the credits. You can use these credits in future years when the company generates income tax liability. You can carry forward credits for up to 20 years.

If you file the tax return on time without Form 6765, you have two options to report these carry-forward credits:

Option 1: Amend the prior year's return to include Form 6765, claim the credit, and report the credit balance as a deferred asset on the balance sheet. The IRS does not require Declaration Statements when you amend your return to include credits that you carry forward for future use.

Option 2: Simply report the credit balance on a carry-forward schedule. Do not file an amendment.

To use the R&D credit to offset payroll taxes, file Form 8974 with your quarterly payroll tax returns (Form 941). Submit this form to your payroll provider to add the credit to your payroll tax return.

The credit applies against employer payroll taxes quarterly, beginning the first calendar quarter after you file your federal income tax return.

To receive your credit quickly, timing is everything. File Form 6765 with your tax return. Keep these dates in mind:

End-of-quarter deadlines: Payroll offset can begin the quarter after you file. So if you claim R&D tax credits to offset your payroll taxes, file before the end of the quarter, on or before your IRS filing deadline.

Q1: March 31

Q2: June 30

Q3: September 30

Q4: December 31

Federal tax filing deadline: By entity types with a calendar year-end of 12/31.

S-Corp, Partnership

March 15: On time

September 15: Extended

C-Corp, Sole Proprietorship

April 15: On time

October 15: Extended

Any entity with a Fiscal Year End of September 30

September 15: On time

April 15 (of the following year): Extended

Note: If the Federal tax deadline falls on a weekend or holiday, the deadline moves to the next business day.

IRS turnaround

10–12 weeks (estimate)

You can use R&D tax credits in three ways: payroll offset, liability offset, or carry-forward credit.

How your business uses the credit depends on many factors. We'll help you determine which method is right for your business.

Payroll offset is an option for companies that meet the IRS's "startup rules." These companies can use R&D credits to offset their payroll taxes, specifically the employer-paid portion of the Social Security and Medicare tax. To qualify as a startup, your company must meet two rules:

Rule 1: Your company has less than five years of gross receipts/sales.

Rule 2: Your company has less than $5 million in gross receipts/sales in the tax year for which you claim the credit.

Note: After the fifth year, you cannot use the payroll tax offset. The offset option is limited to a tax return or superseding tax return that's filed in a timely manner.

How we apply R&D tax credits

We apply your R&D tax credits directly to your account. Upload a copy of your filed tax return to your R&D dashboard. Make sure it includes Form 6765, which we provided. Also, make sure the copy shows the filing date. We apply the credits to your payroll taxes and help you file the quarterly forms.

Payroll offset starts reducing your payroll taxes the quarter after you file. You must claim it on tax returns filed by the original IRS deadline or under extension.

Claim R&D credit as a payroll offset in real time

You can easily apply your R&D payroll offset credits with Gusto. After you file your return with the Form 6765 our team provides, upload it to your R&D portal. Our team reviews your filing and applies the credits for use in the quarter after you filed.

You can only claim one year's credit at a time until you use the full amount.

In 2023, the IRS updated guidelines to allow R&D tax credits to apply to employer Medicare after you exhaust employer Social Security. For now, we will not apply real-time credits to Medicare. We'll report Medicare credit amounts on quarterly filings, and the IRS will refund you.

Important: The option to claim the credit in real time only appears in your account if you have a remaining balance to apply. When you can claim also depends on when your accountant filed your most recent business income tax return. You can claim the credit starting the first day of the quarter after filing. For example, if your accountant filed your return in May, the credit period begins July 1 (the first day of the next quarter) and runs through June 30 of the following year.

Check R&D credit usage

To check your R&D credit usage:

Click Reports.

Select the Federal R&D tax credit option.

You'll find the exact breakdown and usage of your credits.

To check real-time credit use, compare the tax totals on your payroll history to the total taxes debited in your cash requirements summary. This shows we did not debit the employer-paid Social Security taxes.

Profitable companies, like C-Corps and Sole Proprietorships, can use R&D credits to offset some or all of the business tax they owe when filing.

Profitable pass-through companies, like S-Corps and Partnerships, can apply R&D credits to offset personal income tax for their shareholders, partners, or LLC members.

A pass-through entity is a business where profits flow through to its owners or members. This profit is taxed as individual income. These businesses do not pay income taxes at the business level.

If you do not have taxes to offset in the tax year or your company is not profitable, you can carry forward both federal and state R&D credits. Carry-forward credits remain a deferred asset on your company's tax return balance sheet until you can use them against future tax liability.

You can also apply your current R&D tax credits to prior-year tax liabilities by amending the prior-year return.

Reminders

You can carry forward federal credits for up to 20 years.

Each state has its own rules about credit expiration.

Example: California's state credit can be carried forward indefinitely.

You can also carry back the R&D tax credit for one year to apply the credit retroactively by amending the prior year return.

When you claim R&D tax credits, you need comprehensive documentation to prove eligible R&D activities.

The documentation confirms that your company used science and technology to create something new or improve existing products or processes.

Required documentation for R&D tax credit claims

Supporting documents are documents that originated during the development year and prove that you meet the four-part test. We suggest organizing your documents by business components and tax year.

Supporting documentation for four-part test criteria:

R&D four-part test category

Sample document types

Business Component / Permitted Purpose

Project management summaries, technical specifications, whitepapers, new feature releases, brochures, pamphlets, press releases, and other similar documents

Technological Uncertainty

Meeting minutes, project notes, documents submitted to management for research project approval, and emails

Process of Experimentation

Testing reports, experiment records, brochures, pamphlets, annual internal reports, field and lab summaries, progress reports, and published documents

Technological in Nature

Jira tickets, code commits, and technical specifications

Mixed categories

Patents, contracts, letters of agreement, memoranda of understanding, expense details, and payroll records

R&D documentation best practices

Document the time each employee spent on qualifying R&D activities.

Specify the nature of their tasks and the percentage of time spent on R&D.

Document the experimental process, like hypotheses, testing methods, and outcomes.

Highlight when you encountered uncertainties and the steps you took to resolve them.

Link expenses to the R&D project to show you used resources for qualifying activities.

If external parties are involved in your R&D activities, keep detailed documentation of subcontractor agreements and the specific R&D-related tasks they performed.

This includes invoices, contracts, and other relevant documentation.

If you're an Accountant Partner with Gusto, help your clients discover, claim, and use R&D tax credits

To refer your clients to Gusto's R&D tax credits:

On the left, click Refer & Earn.

Click R&D Tax Credits.

Select Get Started.

Share the referral link with your client.

We'll determine if your client qualifies. If they qualify, we'll handle the entire study and provide the documentation you need to file.

When your client qualifies for the R&D credit, we'll provide the revenue share and send you a referral gift card.

We charge 15% of the R&D tax credits we find. If we cannot find credits, you pay nothing.

Choose from two payment options:

Pay in 12 equal installments

Pay one lump sum and get an additional 15% off the total price

Our service fees include the complete R&D tax credit calculation and the credit form you need for your filing. We also provide access to our filing guides and documentation to support the credit calculation. If you use your credits to offset payroll taxes through Gusto, our fee also includes help from our team to apply your credits in Gusto and 12 months of the Gusto real-time feature for free ($1,200 value).

Payment timeline

We issue Gusto R&D Tax Credit Service invoices during the first week of the month. You get your invoice starting the month after you approve the report. If you choose a 12-month payment plan, you get invoices at the beginning of each month for 12 consecutive months.

Payment options

According to our Terms of Service, we need permission to ACH debit your Gusto account. We directly debit your account for the service fees after you approve the R&D tax credit report. We do not accept credit card payments. To update the ACH debit account, contact us at [email protected] with new bank details.

Q: Is the R&D tax credit taxable income?

A: No, the R&D tax credit is not taxable income. The credit as non-dilutive capital for your business.

Q: What if I already claimed the R&D credit for this tax year?

A: If another party calculated the credits (like your CPA or another R&D firm), your accountant or someone with accountant access to your Gusto account can apply the credits for redemption.

Q: What if I claimed R&D credit in previous years?

A: If you claimed the R&D credit in prior years, make sure to provide Form 6765 for all applicable tax returns when you onboard to our R&D tax services. Our team needs this information when we calculate your current year's credits

Q: Can I claim R&D tax credits retroactively for past tax filings?

A: Yes, if the statute of limitations has not passed, you can claim R&D tax credits that offset income tax liability retroactively. This option is only available for profitable companies.

You may need to file an amended tax return if you paid tax in past years. You cannot claim R&D tax credits that offset payroll taxes (for early-stage startups) retroactively, but you can carry them forward as a deferred asset on your balance sheet.

If you want to amend a prior year's tax return to claim the R&D tax credit, email [email protected].

Q: Can I unsubscribe from Gusto's R&D emails?

A: Yes, email [email protected] to unsubscribe.

Q: Can I get a non-disclosure agreement (NDA) signed before releasing my info to Gusto?

A: Yes, we provide NDAs. Email [email protected] for more information.

Q: How can I apply my R&D credits that Gusto did not find?

A: If a third-party provider (your CPA or another R&D firm) calculated the credits, your accountant or someone with accountant access to your Gusto account can apply the credits for redemption.

Q: What if I already have an accountant or CPA? Can they claim R&D credits for me?

A: We can work with your accountant to calculate and claim your R&D tax credits. Our technology automates the process by scanning your payroll and accounting data for qualifying credits. This saves you and your accountant time. We'll also help review your claim, assist you or your accountant through filing, and provide support in case of an audit.

Q: My CPA said I do not qualify, but Gusto says I do.

A: Our qualification follows the IRS guidelines in the four-part test. We evaluate qualifications based on the information you provide. We recommend consulting your CPA to determine whether claiming the R&D tax credit fits your circumstances. They may have access to more relevant information.

Q: Can I get R&D tax credits for state tax filings?

A: Yes, but our software currently calculates R&D tax credits only for California.

Q: What's the difference between an amended return and a superseding return?

A: You file a superseding return after the originally filed return and within the filing period (including extensions).

You file an amended return after the originally filed or superseding return and after the filing period expires (including extensions).

If you want to amend a prior year's tax return to claim the R&D tax credit, email [email protected].

Q: I'm changing payroll providers. How do I take my payroll tax credits with me?

A: Contact your new payroll provider to ask how you can use your remaining credits with them. They need a copy of your most recent Form 8974 and Form 941. You can find these in your Gusto account under Tax documents.