Set up and manage life insurance (for admins and employees)

This article explains how Primary admins and full-access admins can set up life insurance for their company, how employees can add beneficiaries, and how life insurance affects taxes.

Basic life insurance pays a sum of money to a beneficiary if the policyholder passes away. Some policies also pay out if certain accidents happen during the coverage period.

You can offer life insurance through Gusto or add an external policy to your Gusto account.

Offer life insurance with Gusto

Primary admins and full-access admins can view quotes and apply for insurance benefits at any time. You must offer medical coverage through Gusto before you can offer life insurance or other benefits.

When your company offers life insurance through Gusto, we automatically enroll all eligible employees. The policy is non-voluntary, meaning the company pays 100% of the premium, and all eligible employees are automatically enrolled. Dependents cannot enroll.

Set up deductions for an external life insurance policy

If you offer group term life insurance through a broker outside of Gusto, you can add the benefit to Gusto. This lets you record taxes and collect any employee contributions.

Add life insurance to payroll

To record a life insurance benefit in your company account:

Go to Benefits.

Scroll to Financial health.

Click Show more financial health benefits.

Next to Group Term Life Insurance, click Set up.

Select Yes, we currently offer this benefit.

Click Next.

Add a name for the benefit. This name will appear on employee paystubs.

Enter the employee deduction per pay period.

If employees pay different amounts, enter a placeholder amount for now. You can change deductions after you create the benefit.

Enter the coverage type and amount.

We do not record what the employer pays, if anything. Employees only pay taxes on coverage over $50,000. They do not pay taxes on what the employer pays. We automatically calculate and apply taxes based on the coverage amount you enter.

Select whether coverage is a flat amount or based on salary. If it’s based on salary, enter the multiplier.

Click Save & continue.

Select the employees this benefit covers. You can change their deductions or coverage amounts after setting up the benefit.

Click Save.

Customize the benefit for each employee

After you add life insurance to your company account, follow these steps if employees have different deductions or salary multipliers.

To change benefits for individual employees:

Go to Benefits.

Under Manual payroll deductions, click the name of the benefit you set up.

Find the name of an employee and click Edit benefit.

Change their deduction, coverage type, or coverage amount.

If you need to make any further changes, click Use custom group term life settings. You can enter a custom taxable income amount. You can also make it so deductions will not reduce the taxable income amount.

Click Save.

When you enroll in a life insurance policy, you can add a beneficiary right away or later. A beneficiary is someone who will get the life insurance money if the policyholder passes away.

Know this before you choose your beneficiaries:

Beneficiaries must be 18 or older to claim a life insurance benefit. If you choose someone under 18, they must be at least 18 years old when they make the claim. Or they need a guardian and a trust set up through your state court (we will not set this up for you).

You can have up to 5 beneficiaries on your account. You can give each person a different percentage, like Alex gets 80% and Jordan gets 20%.

Rules about who you can list as your beneficiary vary by carrier and state. These rules cover things like age and where they live. We keep the beneficiaries you provide on record. But make sure to check with your insurance carrier that your beneficiaries are eligible to receive the benefit.

Add a beneficiary in Gusto

If your company has a life insurance policy managed by Gusto, you can add one or more beneficiaries when you first enroll in benefits. You can add or change beneficiaries at any time.

To add a beneficiary:

Go to Benefits.

Click the Life tile.

Go to the Beneficiaries & Distribution tab.

Click Add beneficiary.

Add your beneficiary’s details.

Click Save.

To add more beneficiaries, click Add beneficiary again, then set the distribution percentage.

If the insured person passes away, the carrier will contact Gusto for beneficiary information. Each time you change a beneficiary, we will use the most recent update to give out the policy benefits.

Change a beneficiary

You can edit a beneficiary’s information or change to a different beneficiary at any time.

To change a beneficiary:

Go to Benefits.

Click the Life tile.

Go to the Beneficiaries & Distribution tab.

Click Edit for the beneficiary you’d like to change or update.

Here you can edit the first name, last name, relationship, or birth date.

Click Save.

Change the payout split

You can edit the percentage split at any time.

To change the payout split:

Go to Benefits.

Click the Life tile.

Go to the Beneficiaries & Distribution tab.

Under Payout Distribution, click Change Contribution.

Update to your desired percentages. The total percentage across beneficiaries must add up to 100%.

Click Save.

Your life insurance coverage may affect your taxes and what appears on your paystub. Whether you owe taxes depends on your coverage amount.

Life insurance policies of $50,000 or less

If your employer pays for your group life insurance and the coverage is $50,000 or less, you will not owe any taxes on it.

This coverage will not appear on your paystub or W-2 because it’s tax-exempt. Only coverage over $50,000 needs to be reported for tax purposes.

Life insurance policies over $50,000

If your life insurance coverage is over $50,000 and your employer pays for it, the amount over $50,000 counts as a taxable benefit. This means:

You do not pay taxes on the first $50,000.

You do pay taxes on the cost of coverage above $50,000. This is called imputed income.

The extra taxable amount may appear on your paystub or W-2.

How the IRS calculates the taxable amount

The Internal Revenue Service (IRS) uses a table to figure out how much your extra coverage is worth. The table shows the cost of each $1,000 of extra coverage per month. We add that cost to your federal taxable income. This is based on:

How much coverage you have over $50,000

Your age

How much your employer pays

You can find the full IRS table in the IRS Employer’s Guide to Fringe Benefits. We also included a copy of the 2026 version below.

Cost per $1,000 of protection for one month

Age

Cost

Under 25

$0.05

25 through 29

0.06

30 through 34

0.08

35 through 39

0.09

40 through 44

0.10

45 through 49

0.15

50 through 54

0.23

55 through 59

0.43

60 through 64

0.66

65 through 69

1.27

70 and older

2.06

Source: IRS Employer’s Guide to Fringe Benefits (2026)

Example calculation

John’s life insurance policy covers $200,000. He is 45 years old. His employer pays the full premium. John does not need to pay federal taxes on the first $50,000 of coverage. But he will still pay federal taxes on the extra $150,000 of coverage. The total cost we include in John’s federal taxable wages would be $270 per year (0.15 x 150 x 12).

Note: If an employee is contributing to a life insurance policy, contributions will default to post-tax deductions unless otherwise specified. Learn more from the IRS.

If you add your life insurance policy to Gusto, we calculate tax implications automatically for anyone you mark as a 2% or greater shareholder. This works whether you set it up through Gusto directly, via the broker integration, or the deductions you entered.

Read below if you want to learn why we tax 2% shareholders on life insurance and how we calculate the taxable amount.

IRS rules for shareholders

The IRS usually lets employers provide up to $50,000 of group-term life insurance coverage to their employees tax-free. This means for most employees, the cost of this basic coverage is not included in their taxable income.

For employees who own 2% or more of an S-Corporation, this exemption does not apply. If your company pays for life insurance for all employees, shareholders who own 2% or greater will owe taxes on the full cost of their coverage.

How this looks on paystubs and payroll journals

Here’s where the tax implications for shareholders show up on payroll:

On the shareholder’s paystub: We add the cost of the life insurance to their imputed income. It’s taxable as wages.

On the Payroll Journal report: We include the cost of a shareholder’s life insurance as a separate line item, labeled as imputed pay.

How we calculate imputed pay

We base imputed pay for life insurance on the shareholder’s age, the coverage amount, and the frequency of your company’s payroll runs. If you want to understand how we calculate the value of a shareholder’s life insurance, this is the formula:

(The age-based IRS rate × Coverage amount in thousands × 12 months) ÷ Number of pay periods in a year = Total amount of imputed pay we add to each regular paycheck.

For example:

If a shareholder is 45 years old, their age-based IRS rate for 2026 is $0.15 per $1,000 of coverage.

If it’s a $50,000 policy, the “coverage amount in thousands” is 50.

The yearly cost is $0.15 × 50 = $7.50 per month. Multiplied by 12, this is $90 per year.

If split over 26 pay periods (assuming the company has a bi-weekly pay schedule), we add about $3.46 to a 45-year-old shareholder’s taxable income as imputed pay every paycheck.

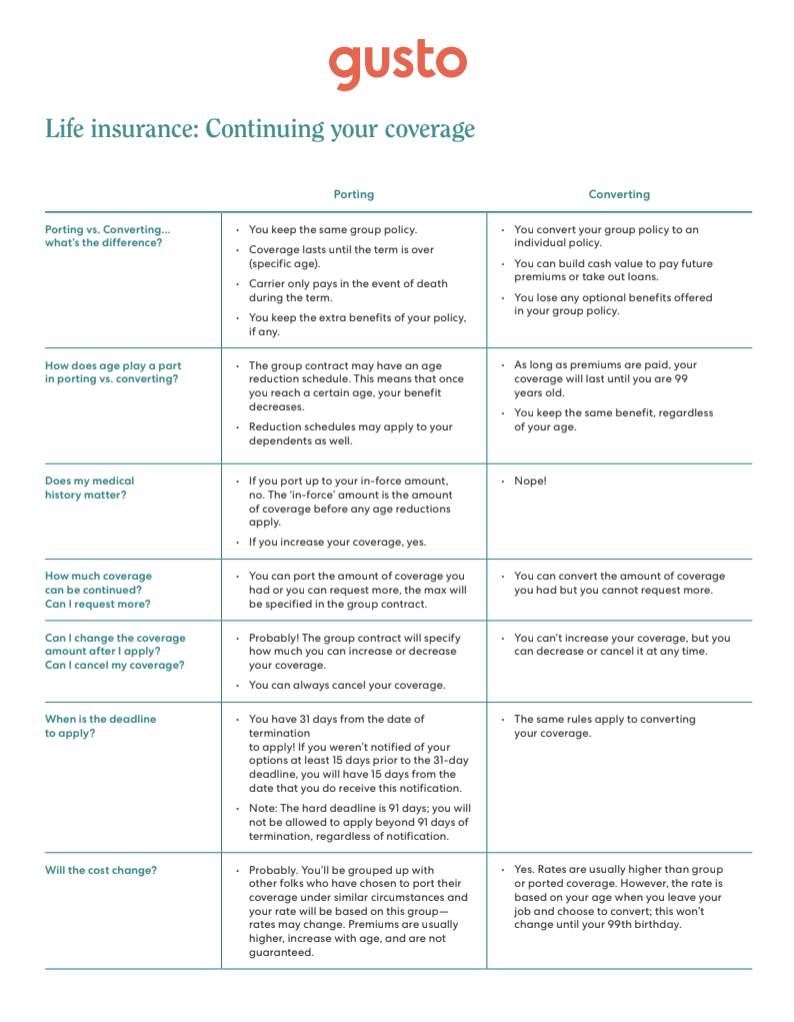

If we manage your policy and you leave your job, we’ll email you with your options to keep your life insurance policy.

If you decide to keep your policy, you can either port or convert the coverage to a new one. Once you decide, contact your insurance carrier for the next steps. Sign in to your carrier’s member website or call the number on the back of your insurance card. You need to send your application to the carrier within 31 days of the end of your employer’s coverage.

Porting vs. converting coverage

Porting means you keep your group policy after you leave your job. Converting means taking your group policy and turning it into an individual policy.

Use the following chart to help you decide whether to port or convert your coverage: